Author: Ignacio López Martín, founder and chairman of Capflex Energía, founder and CEO of Eolinet Renovables.

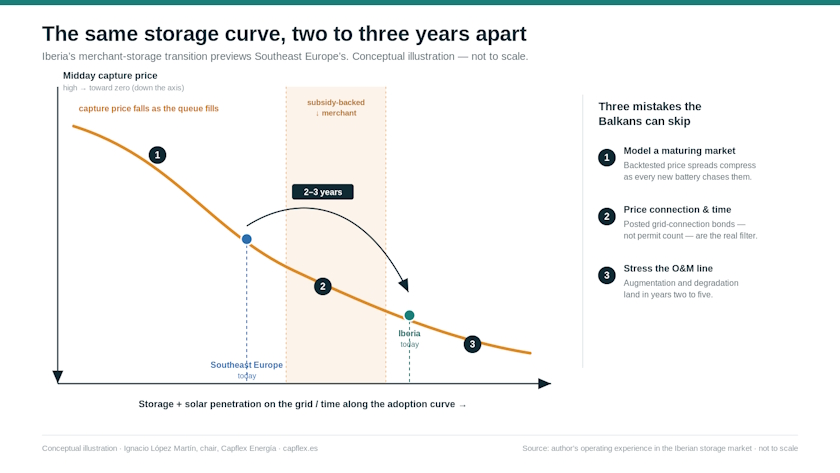

Iberia is two to three years ahead of the Balkans on the same storage curve. An operator who has posted the bonds on Spanish projects points to the three mistakes Southeast Europe doesn’t have to repeat.

Bulgaria already has the largest share of batteries in its power mix in the region. SEEPEX has printed negative prices. HROTE and the EBRD are openly designing BESS incentive models. Across Southeast Europe the message has shifted from “if” to “when” — storage is no longer optional.

I have seen this exact film before. In Spain, just two or three years earlier.

The Iberian grid filled with solar faster than the network could absorb it. Midday prices collapsed toward zero. Subsidy-backed storage gave way to merchant storage. And a generation of developers and investors learned three expensive lessons financing that transition. Southeast Europe is now walking onto the same curve — with the rare advantage of being able to watch where the people ahead of it stepped wrong.

I write as an operator, not an analyst. I chair Capflex Energía, a standalone battery developer with a self-developed pipeline of more than 500 MW in Spain, with grid-connection bonds posted at real nodes. I also run Eolinet Renovables, a wind-blade drone services company starting a proof of concept with a major utility this year. Before that I co-founded an EV-charging platform that went through two industrial due diligences — sold to Shell in 2022, acquired from Shell by Acciona Energía in 2025. The lessons below cost real money. They don’t have to cost yours.

1. Don’t model merchant revenue on a backward-looking curve

Every storage model starts the same way: take the historical price spread, assume two cycles a day, apply a haircut, call it conservative.

It isn’t conservative. It’s incomplete — and in a market that is still forming, it’s dangerous.

The spread you backtest is the spread your own asset class is about to compress. Every megawatt of storage that connects chases the same midday-to-evening arbitrage you did; capture rates fall as the queue fills. In Spain the developers who underwrote yesterday’s spreads into a ten-year model are the ones now revising their returns downward. Southeast Europe’s spreads today look wide precisely because there is so little storage. They will narrow the moment the pipeline everyone is talking about actually energizes.

The fix is not pessimism. It’s building the revenue model around what the asset can capture as the market matures, not around a screenshot of last year’s volatility — and treating route-to-market, balancing exposure and who actually sits at the trading desk as an operating capability, not a spreadsheet line.

2. Don’t underprice grid connection and permitting

In Spain the single most underestimated number was never the battery cost. It was time — and the cost of holding a position while time passed.

The mechanism that separates a real project from a paper one is the grid-connection bond: capital a developer must post, in cash or guarantee, to hold a node. Posting it is a balance-sheet decision; walking away means losing it. That filter splits any “pipeline” headline into two very different things — projects where someone has money at risk, and projects that exist as a permit on a server. The second category is almost always the majority.

Southeast Europe is now designing exactly these rules — connection regimes, auction and incentive frameworks, the EBRD-backed models in discussion. Whatever shape they take, the lesson from Iberia is the same for both sides of the table. For developers: assume connection and energization take longer than the official timeline, and capitalize for that delay from day one. For investors: diligence the bonds and the connection milestones, not the permit count. A pipeline with nothing posted is a watchlist, not an asset.

Get this wrong and you don’t lose a project. You lose the years of carrying cost before you ever earn a euro.

3. Don’t treat O&M as an afterthought

This is the one the whole industry gets wrong, and the one I see most clearly because I operate on both sides of it.

In most models, battery O&M is a flat percentage copied from a solar template. That number survives exactly until the first augmentation conversation. Storage O&M is not solar O&M: it is degradation management, augmentation capex disguised as opex, firmware and battery-management-system dependency on a single supplier, and an insurance market still deciding what it thinks about thermal risk. None of it behaves like a flat percentage, and most of it lands in years two to five — conveniently outside the holding period most investors stress hardest.

I see the same blind spot in wind, where my other company inspects and cleans turbine blades for utilities. The industry systematically underprices the boring, recurring, operational line — and then acts surprised when it becomes the bottleneck. The tightening rules on blade waste across Europe didn’t create that problem; they exposed it.

Storage in Southeast Europe is walking into the same lesson with even less operating history to lean on. If you are underwriting a BESS project here, stress the O&M line the way you stress power prices. Almost nobody does. Everybody should.

Close — the advantage of going second

None of this is a warning to slow down. Spain’s build-out is real, the assets are getting built, and I am long the market with my own capital. Southeast Europe’s direction — Bulgaria’s lead, the HROTE and EBRD work, the honest admission that storage is no longer optional — is exactly right.

The advantage of arriving on the curve a few years late is that the mistakes ahead of you are already documented. Model revenue for a maturing market, not a scarce one. Price connection and permitting time honestly. And treat operations as a margin lever, not a footnote. Do those three things and Southeast Europe can compress into a couple of years what cost Iberia a painful, expensive cycle to learn.

The winners here will be the same as in Spain: the teams that pair capital with operating discipline early. That discipline is scarce, which is exactly why it pays.

About the author

Ignacio López Martín is founder and chairman of Capflex Energía, a standalone battery-storage developer in Spain with a self-developed pipeline of over 500 MW, and founder and CEO of Eolinet Renovables, a drone-based wind-blade services company beginning a proof of concept with a major utility in 2026. He previously co-founded Cable Energía, an Iberian EV-charging platform sold to Shell in 2022 and acquired by Acciona Energía in 2025.