Photo: Freepik

The mature residential battery storage markets in Europe are stabilizing, while policy-driven and emerging markets are gaining traction, according to EUPD Research. Its new report showed prices of home batteries slumped more than 50% between the first half of 2023 and the first half of this year.

The European residential battery storage market has remained resilient in 2025, with notable growth across mid-sized and emerging markets, according to EUPD Research’s latest Electrical Energy Storage (EES) Report. It tracked systems of up to 20 kWh.

While mature markets such as Germany and Italy began the year with more subdued figures, the overall market trajectory points to continued expansion, with over one million new residential storage systems expected to be installed across Europe this year. Although the phaseout of subsidies and adjustments to support schemes led to a weaker start in top markets, the outlook for the second half is more optimistic, the firm said.

Home batteries are overwhelmingly intended for storing electricity from household photovoltaic systems, usually installed on roofs, balconies or on canopies next to houses.

Dynamic electricity tariffs, self-consumption fueling residential battery storage push

Increasing interest in dynamic electricity tariffs and enhanced self-consumption is expected to stimulate demand for residential market storage. Mature markets are stabilizing, while policy-driven and emerging markets are gaining traction, the update showed.

The sector continues to benefit from falling battery prices. A significant drop in lithium prices, combined with intensified competition due to the influx of new market players in the past two years, has accelerated price erosion and reduced overall system costs.

The data provider’s price index more than halved between the first half of 2023 and the first half of this year. The current average selling price of residential battery storage, in the second half of 2025, came in at EUR 711 per kWh. It is 46.6% lower than in the first half of 2023.

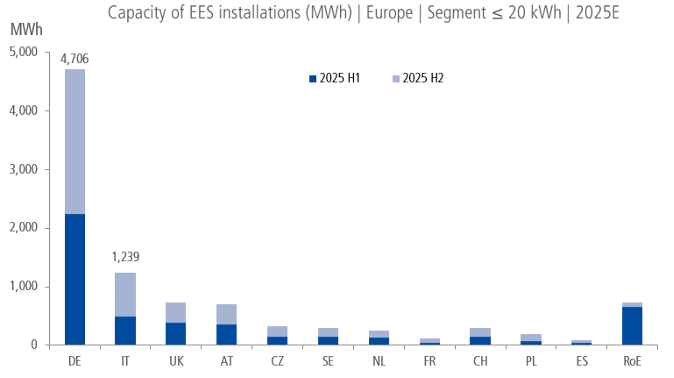

The segment of newly installed residential battery storage in Germany is in a moderate decline

Despite a moderate decline in residential battery installations during the first half of 2025, Germany remains the strongest market in Europe, with demand expected to stay resilient throughout the year. The projected 6% year-on-year decline is mainly due to slower deployment of photovoltaics, reduced regional incentives, and a growing shift in focus toward commercial and industrial (C&I) and utility-scale storage.

Alongside Italy, Germany is estimated to account for the lion’s share of new residential storage capacity additions through 2028, despite Italy’s current slowdown amid the gradual weakening of the Superbonus scheme.

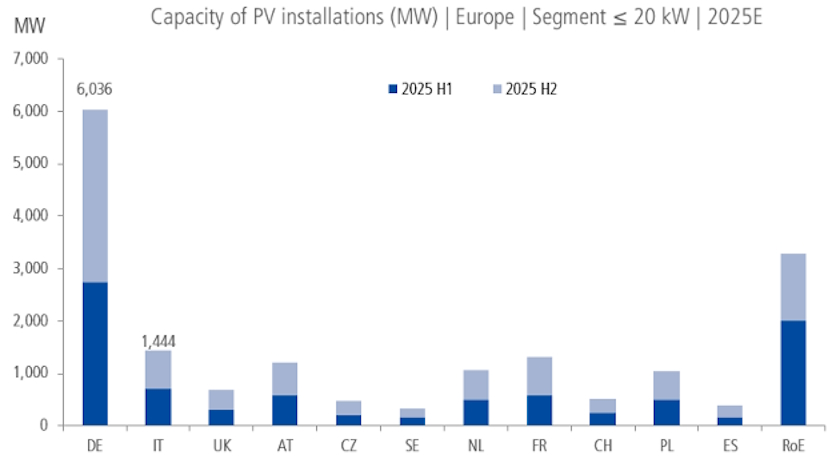

This year’s residential battery storage additions in Europe’s largest economy are seen at 4.7 GWh, compared to a projected 6.04 GW in home PV installations of up to 20 kW. Italy accounts for an expected 1.24 GWh and 1.44 GW, respectively.

Steady, robust growth in several markets

Markets such as Austria, France, the Netherlands, and the Czech Republic are demonstrating steady and robust growth, driven by rising electricity costs since 2023, increasing PV adoption, stable policy support, and increased awareness of the benefits of energy independence.

Sweden, bolstered by tax rebates and a national push toward energy self-sufficiency, has seen a record number of PV systems being installed with residential storage.

As for equipment providers, BYD maintained its top position in 2024, capturing a 20% market share, which is expected to reach 21% this year.

Be the first one to comment on this article.