Photo: iStock

Despite the surge in planned projects for the production of critical minerals such as copper and lithium, more work is needed to ensure a diversified and sustainable supply to support the energy transition, the International Energy Agency found in a new report.

The market for materials necessary for electric vehicles, wind turbines, solar panels and similar technologies has doubled in size in the five years through 2022, to USD 320 billion, IEA said in Critical Minerals Market Review 2023. Its first annual report for the segment points out that bulk materials like zinc and lead saw modest growth.

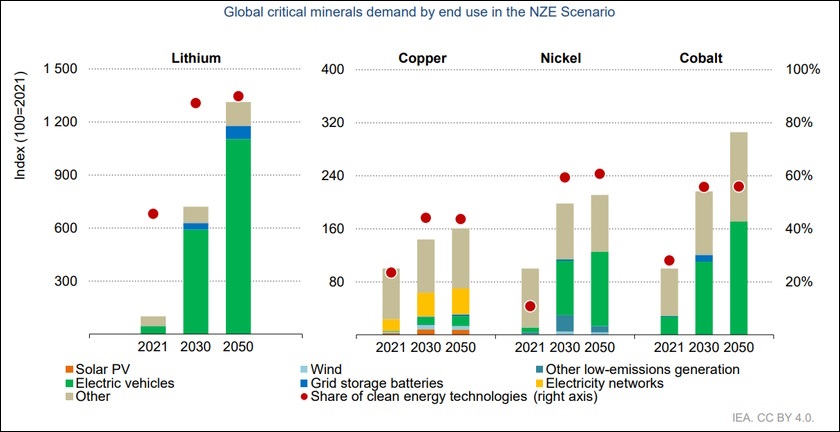

In the net zero emissions scenario, the demand for critical minerals grows 3.5 times by 2030.

Rising demand and high prices of key energy transition minerals are mainly attributed to the energy sector. The demand for lithium has tripled compared to the 70% rate for cobalt and 40% for nickel. In response, investment in critical mineral development rose 30% last year, following a 20% increase in 2021. Among the different critical minerals, lithium saw the sharpest increase in investment, 50%, followed by copper and nickel.

Current projects do cover national pledges but it’s not enough for climate neutrality

“At a pivotal moment for clean energy transitions worldwide, we are encouraged by the rapid growth in the market for critical minerals, which are crucial for the world to achieve its energy and climate goals,” said IEA Executive Director Fatih Birol. “Even so, major challenges remain. Much more needs to be done to ensure supply chains for critical minerals are secure and sustainable.”

More projects will be needed by 2030 to stay on the net zero emissions path

If all planned critical mineral projects worldwide come to fruition, supply could be sufficient to support the national climate pledges announced by governments, according to the IEA’s analysis. However, the risk of project delays and technology-specific shortfalls leave little room for complacency about the adequacy of supply.

In any case, more projects would be needed by 2030 in the net zero scenario – NZE, in which global warming is limited to 1.5 degrees Celsius, the agency warned.

Copper

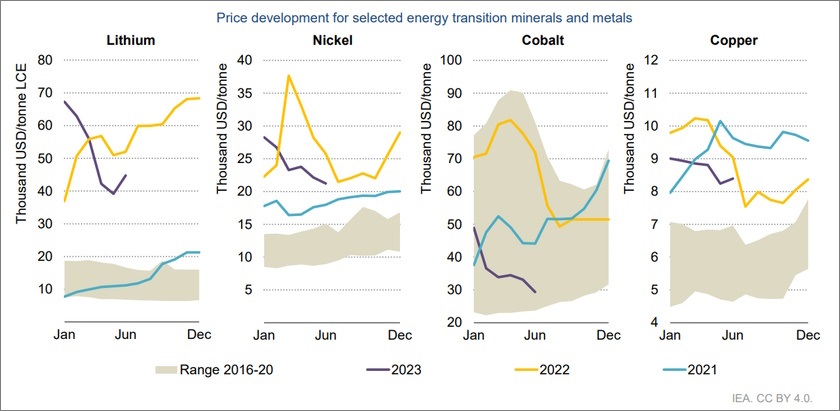

Since the second half of 2022, copper prices have been trending downwards, although they were occasionally propped up by supply disruptions in Chile and Peru, expectations for the reopening of China’s economy and low inventory levels.

Prices have continued to fall in the first few months of 2023 as new supplies came online while Chinese demand remains subdued. The report’s authors expect a surplus this year and next but also that the production growth rate would decelerate after that.

Lithium

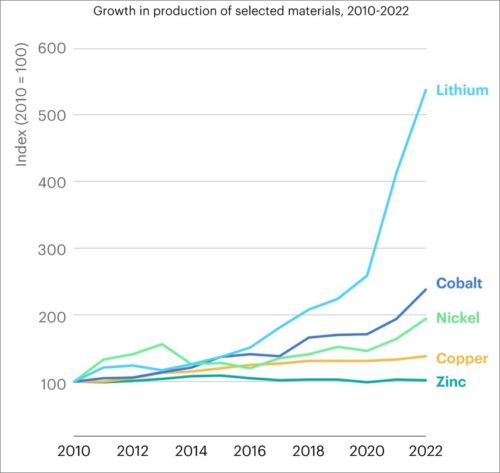

In just a decade, the lithium industry has undergone a drastic transformation, with batteries now being the dominant use of lithium. Demand doubled from 2017 to 2021. Lithium consumption witnessed an additional 30% growth last year. Annual output growth rate ranged between 25% and 35%.

The annual lithium production increase ranges between 25% and 35%

The net zero scenario implies a 422% jump in demand by 2030, to 711,500 tons. The trajectory peaks at 1.37 million tons in 2045, which is ten times more than in 2022.

Recycling of lithium-ion batteries is still in its nascent stages. Today, the vast majority of recycling capacity is located in China, which is also home to the largest electric vehicle fleet and battery manufacturing capacity in the world.

Batteries being recycled today are predominantly coming from consumer electronics and battery manufacturing scrap, but the balance is seen shifting to used batteries when massive batches start reaching the end of life.

Nickel

Nickel, a vital raw material in the production of stainless steel and batteries, has faced challenges of illiquidity in trading and volatility in prices due to its concentration of supply and geopolitical tensions. The industry added a record amount of supply in 2022, with mined nickel production up by 18% and refined nickel production up by 17%.

The surge in supply was primarily driven by Indonesia, the biggest miner, which experienced a staggering 50% growth in both mined and refined nickel supplies, putting the market balance into surplus. In the latter category, it overtook China as the world’s number one.

Cobalt

After reaching a peak of USD 80,000 per ton in March 2022, cobalt prices underwent a consistent downward trend and remained around USD 50,000 per ton throughout the remainder of the year. The muted economic outlook, coupled with China’s stringent lockdown measures, had a detrimental effect on consumer electronics demand, impacting the overall demand for cobalt.

Cobalt prices are expected to remain suppressed throughout 2023

The low demand was additionally impacted by the cost-cutting strategies of Chinese electric vehicle battery producers, opting for cheaper high-nickel chemistries with reduced cobalt content or cobalt-free lithium iron phosphate (LFP) batteries. Cobalt prices are expected to remain suppressed throughout 2023 due to oversupply, IEA said.

Graphite

Composed of layers of graphene, graphite is a material used in multiple industries, from refractory material to lubricant. But demand is growing fastest for its use in batteries.

The prices of natural graphite continue to remain subdued due to weak demand and elevated stock levels. However, production capacity for anodes is exploding, with an announced capacity of 13 megatons per year in 2025, compared with 0.8 megatons in 2021, most of which in China. Graphite production is also increasing but at a slower rate, raising concerns about tight supplies in the coming years, particularly for battery-grade products.

Rare earth elements

Rare earth elements are essential for permanent magnets required by electric vehicles and wind turbines. In 2022 and into 2023, China accounted for 70% of production and 90% of processing.

Weak automotive production and the slowing economic recovery dampened the demand for rare earths last year, resulting in price decreases. The prices recovered to some extent in the latter half of 2022.

IEA includes aluminum, manganese, platinum group metals and uranium in key commodities.

Be the first one to comment on this article.