Photo: Klas_lu from Pixabay

The European Union is set to install less new solar capacity in 2025 than it did last year – the first annual drop in a decade, according to SolarPower Europe.

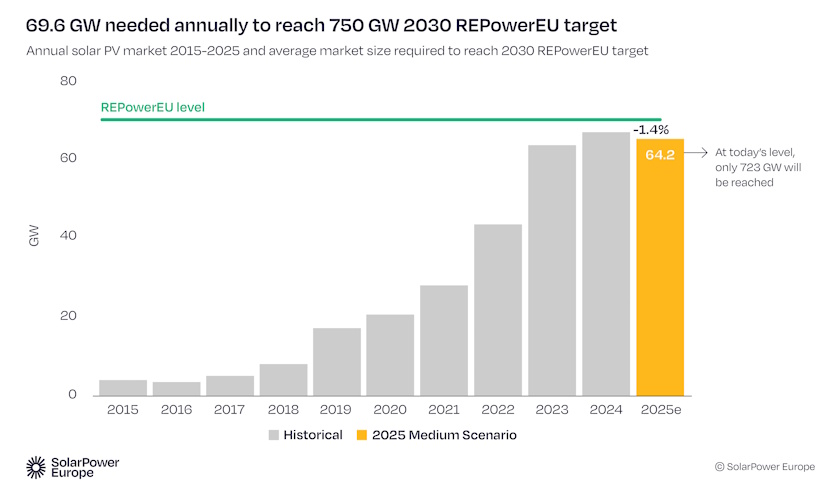

In its mid-year analysis of the photovoltaic market in the EU, SolarPower Europe said new installations are expected to decrease 1.4% this year. It would be the first slowdown since 2015. The market increased by 47% in 2022, by 51% in 2023, and by 3.3% in 2024.

The EU is set to add 64.2 GW, compared to 65.1 GW in 2024, SolarPower Europe said.

The update comes after solar became the EU’s largest source of electricity for the first time, in June 2025. According to Ember, photovoltaics generated 22.1% of EU electricity (45.4 TWh) last month, more than any other power source. In absolute terms, it was a year-over-year increase of 22%.

Dries Acke, Deputy CEO of SolarPower Europe, said the 1.4% decline may seem small, but that the symbolism is big. In his view, a market decline, right when solar is meant to be accelerating, deserves EU leaders’ attention.

“Europe needs competitive electricity, energy security, and climate solutions. Solar delivers on all of those needs. Now policymakers must deliver the electrification, flexibility and energy storage frameworks that will drive solar success through the rest of the decade,” Acke stated.

The European Commission’s 2025 target for overal PV capacity is 400 GW, while by the end of the year the bloc should host 402 GW. To meet the 2030 target, and deliver the continent’s decarbonisation and competitiveness goals, Europe must install nearly 70 GW per year through the rest of the decade, according to SolarPower Europe.

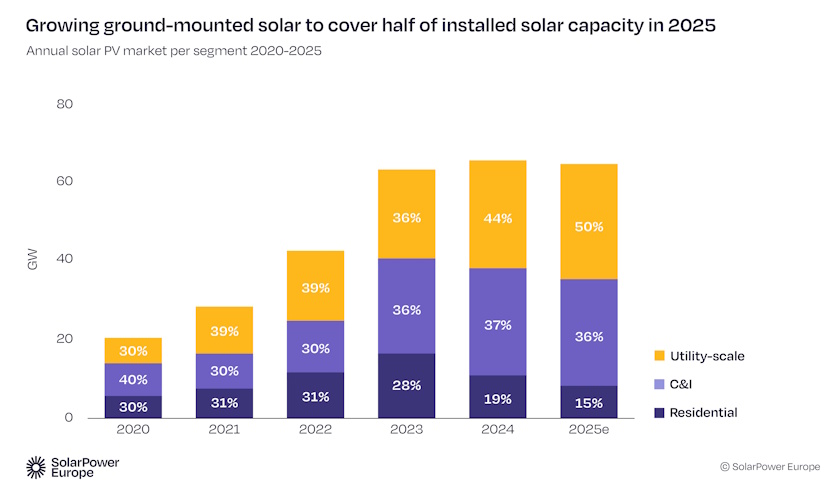

Rooftop segment is shrinking

The projected decrease in solar is driven primarily by a declining rooftop segment, particularly home solar, the report reads.

Traditionally strong residential rooftop solar markets, like Italy, the Netherlands, Austria, Belgium, Czechia, and Hungary, are slowing. Households there are now postponing installations as the impact of the 2022 energy crisis wanes, according to the association.

There is one more reason – a withdrawal of incentive schemes without adequate replacements. It resulted in a residential rooftop market collapse of over 60% versus 2023 in most of the group. Similarly, Poland, Spain, and Germany are experiencing a decline of over 40%. Good news comes from utility-scale solar. It is expected to continue growing and amount to around half of all new capacity additions.

The authors of the outlook attributed the confidence to improved auction design, and the boost in auction-deployed solar from hybrid and co-located storage projects, especially in Germany and Bulgaria. Germany leads in solar auctions, followed by the Netherlands, France, and Italy, with Poland and Ireland also scaling up, the report underlines.

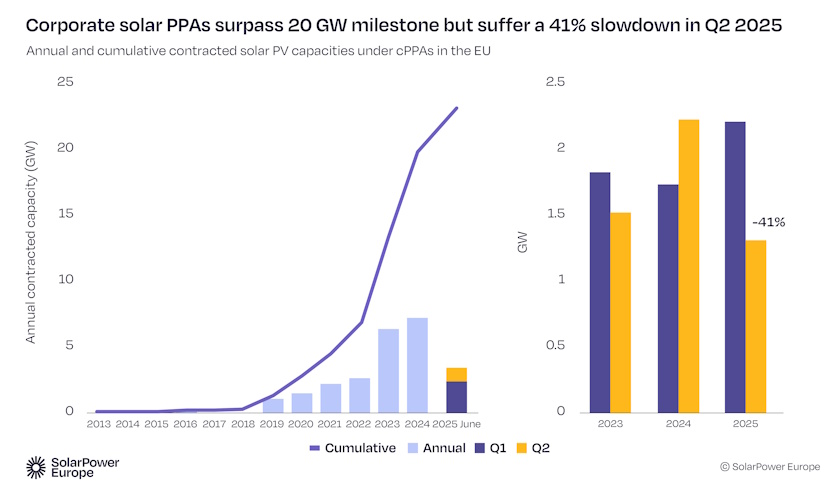

It also points to a weakening in the segment of corporate power purchase agreements (PPAs). They have been a key driver of utility-scale solar in recent years. However, in 2025, falling electricity prices have reduced buyers’ incentive to sign long-term deals.

New solar PPA signings have dropped by 41% in the second quarter of this year against end-March, according to the report.

Be the first one to comment on this article.