Photo: Freepik

The number of power purchase agreements (PPAs) for renewables in Europe fell by 31% and the volume tumbled 26% in the first half of the year from the levels in the same period of 2024, Pexapark found. Germany and France registered sharp declines in the photovoltaics segment, but a surge in Italy and Spain has more than offset the drop.

The meteoric rise in deals for battery energy storage systems, BESS, is a clear sign of its maturity.

In its latest report, analytics and advisory firm Pexapark provided a detailed look into PPAs and contracts for battery energy storage systems in the first six months of 2025. It found that PPA activity shrank by more than a quarter in year-over-year terms, but not everywhere and not due to solar power.

Across 124 deals, 6.08 GW of renewable electricity capacity was contracted in the first half, which is 31% and 26% down, respectively, from the same period of 2024. Conversely, the average deal size advanced 5% to 48.2 MW.

Notably, the April-June period was much weaker than the first quarter of the year, with just 50 deals, but the volumes were almost evenly split.

The main technologies in the first half were solar power, 4.2 GW from 73 deals, onshore wind (1.4 GW and 32 PPAs), mixed technology (290 MW and nine deals) and offshore wind (134 MW and four deals). The result is proportionate to the picture from January through June 2024.

Despite concerns over saturation of demand for standalone solar, volumes have firmed. The 4.2 GW of solar capacity contracted under PPAs compares to 3.9 GW of the first half of last year. The deal count landed at 73, against 95, which is in line with the overall trend.

PPA activity in Germany plunged 84% in terms of volume

Solar offtake activity reveals a clear split in market momentum. It is slowing down in markets where cannibalization has worsened drastically and rapidly – such as Germany and France. In fact, Germany saw the largest decline in volumes – a remarkable 84% year-on-year decrease in terms of overall volumes, with 228 MW across eight deals in the last six months, versus 1.2 GW and 31 deals in last year’s equivalent.

There is stable or even upward appetite in markets which have had time to adjust to cannibalization and the lower valuation of solar production, or where cannibalization levels are still very low

Conversely, solar PPA activity in Italy and Spain spiked, more than making up for the said decline.

“These numbers support the hypothesis that there is stable, or even upward appetite in markets which have had time to adjust to cannibalization and the lower valuation of solar production – i.e., Spain, or cannibalization levels are still very low – such as Italy. Italy’s solar PPA volumes grew 184% year-on-year, with nearly an additional 700 MW procured compared to the same period last year. Corporate appetite in the country is growing, and so is deal size – with a 420 MW solar corporate deal announced in June comprising the country’s largest PPA ever recorded,” the analysis reads.

As for Southeastern Europe, OMV Petrom’s deal with Enery for their joint solar power project Gabare in Bulgaria was Europe’ third-largest PPA in June.

Flexibility monetization is opportunity for market players with right profile

In a market increasingly driven by flexibility monetization, today’s challenges – cannibalization, future capture dynamics and balancing risks – are becoming opportunities for market players with the right profile. And with corporate buyers more hesitant to pay premiums for solar, transactable prices are—perhaps for the first time in a while – closer to perceived fair value, according to the report’s authors.

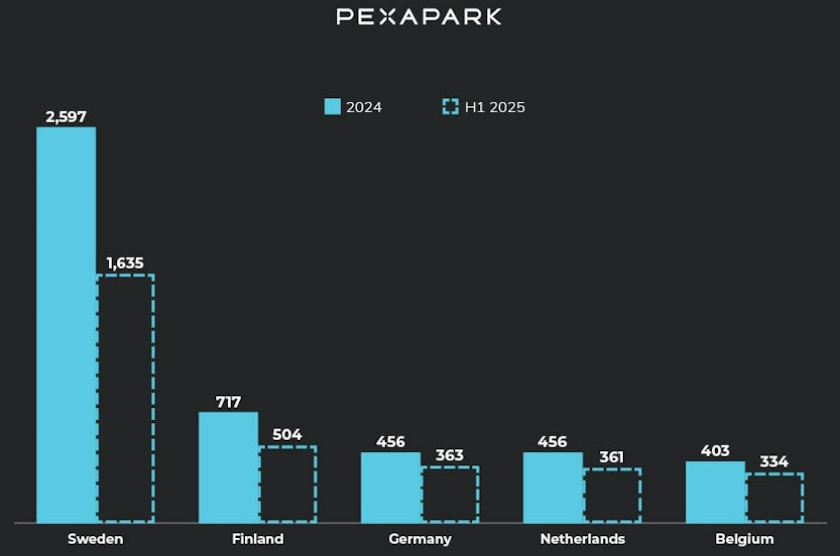

Wholesale electricity prices in Sweden were negative for almost two fifths of the time in the first six months of 2025

Hourly periods with negative prices at wholesale electricity markets continued strong in the first half. Sweden maintained its top position by far, with most such events. There were 1,635 hours with negative prices from January until the end of June. It is a stunning 37.8% share of the entire period and already 63% of the tally from all last year.

The other jurisdictions that make up the top five in Europe: Finland, Germany, the Netherlands and Belgium, remained the same since 2024.

On average, European countries have already reached around 67% of the number of hours counted in 2024 as a whole. Norway hit 90%, Denmark 87% and Spain climbed to 86%, suggesting that last year’s records would fall.

BESS deal volumes already three times higher than in all 2024

The maturity of the BESS industry is clearly reflected in the deal count and contracted volumes over the past 18 months, with the trend increasingly pronounced in 2025.

Battery storage capacity being contracted under optimization or fixed-revenue offtake contracts (so-called floors and tolls, respectively) amounted to a total of 4.6 GW in capability and 9.2 GWh in capacity across 36 deals. It is just over three times more than in entire 2024 in both benchmarks. The deal count was 44% up from all last year.

The lion’s share of the deal count concerns BESS assets with a two-hour duration

The rapid growth was driven by a wave of new agreements in the two most advanced markets – Great Britain and Germany – alongside first-ever BESS deals emerging in Belgium, Poland, Greece, and Bulgaria. The lion’s share of the deal count concerns BESS assets with a two-hour duration, which the ratio of operating power and capacity also indicates.

Pexapark provides of price data, market intelligence, and advisory services for renewable energy. It was one of the knowledge partners at this year’s edition of Belgrade Energy Forum, organized by Balkan Green Energy News.

Be the first one to comment on this article.