By Vojislav Milijić, CEO of Foragrobio CC d. o. o. / president of Serbian National Biomass Association Serbio

E-mail: vojislav.milijic@serbio.rs

Wood pellet is a fuel produced by pelletizing milled wood. Even though the product started to develop in the seventies and the eighties the real wood pellet boom started in 2000. First major plants were developed in Northern, Western and Central Europe. However, with the demand growth in the European market, huge capacities developed form 2005 in Eastern Europe as well and in America from 2010.

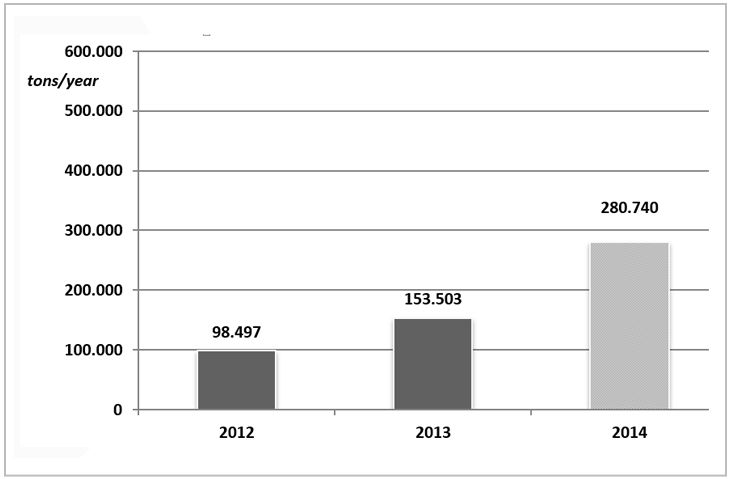

Wood pellet production in Western Balkans started in 2006/07 with development of capacities in Croatia, Bosnia and Herzegovina and Serbia. Development was gradual with few developed factories per year until 2010, when a real boom started in BiH and Serbia, and by 2014 there were over 40 and over 60 producers, respectively. First factories in Montenegro started in 2014. It seemed like anybody with some capital was pursuing locations and wood supply contracts in order to invest in pellet production. In the meantime several plants with production capacities of over four tonnes per hour have either gone bankrupt or switched owners. In case of Serbia in 2014, total capacity exceeded half a million tons per year. But production could barely reach 50% of the capacity. According to the Report on Wood Pellet Production and Market Structure in Serbia from 2014, it was estimated at over 250,000 tonnes, after 150,000 from 2013 and less than 100,000 tonnes in 2012.

Figure 1: Wood pellet production in Serbia http://www.bioenergy-serbia.rs/images/documents/studies/WOOD_PELLET_PRODUCTION_AND_MARKET_STRUCTURE_IN_SERBIA.pdf

This is an increase of more than 150% in two years. However, the growth has stopped in autumn of 2014, and it seems there is a decline from this year and troubles have started for most of wood pellet producers in Serbia and other Western Balkan countries.

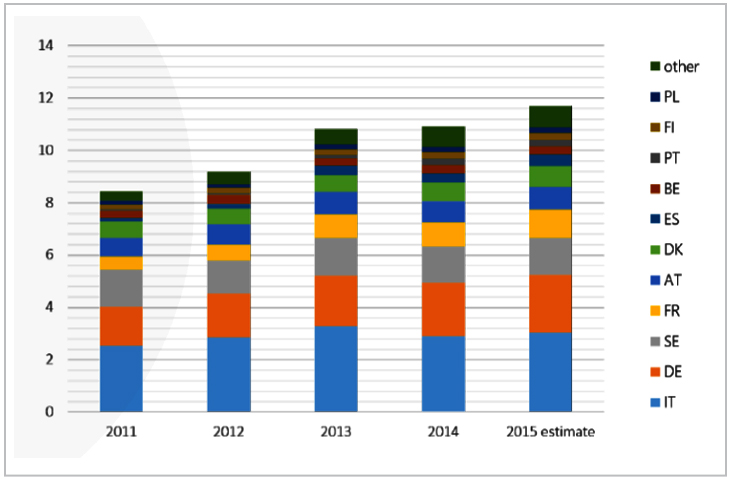

Why is this the case? It is true that demand for wood pellet is rising and total consumption in 2014 in the European Union reached 18.8 million tonnes, but if one looks more closely to the results of EPC survey presented in Aebiom’s statistical report (page 14) it is clear that in fact in most of the countries except Germany (which also has the largest output of wood pellets in the bloc, consuming less than it produces) consumption has decreased in 2014.

Figure 2: Wood pellet consumption in EU28 – http://www.aebiom.org/wp-content/uploads/2015/10/AEBIOM-Statistical-Report-2015_Key-Findings1.pdf

Retreat in Italy

This is especially the case with Italy, where consumption dropped from around 3.3 million tonnes in 2013 to 2.9 million in 2014, and it is questionable if the projection of three million tonnes for 2015 will be reached. On the other side, from 2012 to 2014 over 70% of wood pellet from Serbia (and similar or higher share from BiH and Croatia) was exported. Over 50% of exported wood pellet produced in Serbia was delivered to Italy and additional 15% to Slovenia, while another 15% was exported to Greece, where demand for pellet also dropped due to economic and financial crisis.

But reduced demand is only part of the problem. Bigger issue for Western Balkan producers is the competition from the United States, Canada, the Baltic countries, Belorussia and Ukraine. Last autumn and this winter and spring we had the case that price of wood pellet from America delivered to Italian ports was similar to that in most of Serbian, Bosnian and Croatian factories. And problem with the price is that wood pellet from aforementioned destinations usually comes with better quality.

Beech instead of waste

Can Western Balkan pellet producers be competitive on the global market? Most wood pellet producers in Serbia have the capacity below one tonne per hour, while only 10% have over four tonnes, compared to large-scale factories producing over 200,000 tonnes per year in America, Russia, Romania and some other EU countries. Most of the larger operators in Serbia produce beech wood pellet from long firewood and not from sawmill residues or sawdust. In fact, demand for sawmill residues derived from wood pellet and chipboard factories in Serbia increased the price of residues to the level of firewood. And there isn’t a significant number of small-scale wood pellet factories which utilize their own sawmill residues, while there are only few wood processing companies with serious production which make wood pellet from predominantly sawmill residues.

Picture 1: Example of a modern Amandus Kahl wood pellet line in Vektra Jakic pellet factory in Pljevlja, Montenegro

Producers in other mentioned countries in most cases rely on large-scale wood processing industry and utilize sawmill residues. So their raw material is cheaper, dryer and with less bark or possible ash content. Also, most pellet producers in Serbia and BiH are domestic companies with limited capital and they have installed used pelletizing equipment or lower quality one, so they are faced with increased maintenance costs or additional costs for replacement of equipment. Most of the wood pellet factories in America, Russia and the Baltic countries are owned by large companies with capability to invest in cutting-edge technology.

Economy of scale and ships

Both the quality of wood and the equipment eventually reflect on the quality of the product. There are only seven wood pellet producers in Serbia with En plus A2 certificate and none with En plus A1 or DIN plus. It is really questionable if anybody in Serbia would be able to reach A1 if pellet is made of beech wood with existing equipment. The competition from America and Europe in fact has better investment potential, better equipment, cheaper raw material. The only advantage that Western Balkan producers do have is the lower price of electricity and workforce. But modern pellet factories do not require a significant work force. Next issue is the transportability of wood pellet. While producers from America, Russia and Baltic countries rely on shipping via sea or railway, our producers still rely on trucks in most cases. Therefore, the competition has cheaper transport as well.

Some factories in Serbia now are trying to rely on the domestic market. Domestic consumption has grown to 90,000 or maybe even up to 100,000 tonnes, but it is really questionable if the domestic market can grow more without any subsidies to population for energy efficiency and installation of wood pellet boilers. Wood pellet is comfortable and it may be competitive compared to natural gas, but for markets with limited willingness and purchase power in most of the population, such as in Serbia and other countries in the region, firewood, coal or even electricity remain a more affordable solution.

The perspective of wood pellet production in the current situation for most of Western Balkan producers does not look so bright. It is not hard to foresee that the number of factories will be significantly reduced and that only those who can adapt, enlarge their capacities, reduce their raw material costs, improve product quality and become more efficient will have a chance. And this only if they can find stable and secure market channels.