Europe is now facing a parallel gas and power crisis. The influence of the rising cost of gas driving up power prices is well understood. What is receiving less attention is a rapidly accelerating power crisis which is driving a renewed surge in gas prices.

The geopolitics of Russian supply dynamics is currently dominating global headlines. The current conflict has exposed the extent of Europe’s dependence on cheap hydrocarbons from a hostile neighbour. Russia cutting supply to Europe has been the primary driver of the surge in gas prices across Europe in H1 2022, reads an article by Timera Energy, a London- based consulting company providing consulting advice on value and risk in energy markets.

Europe’s parallel power crisis has gathered pace across the summer. This is being driven by nuclear availability issues, depleted hydro levels & declining thermal output (both due to fuel access issues & plant closures). Power prices across Europe are surging to record levels, now materially outstripping the rise in gas prices.

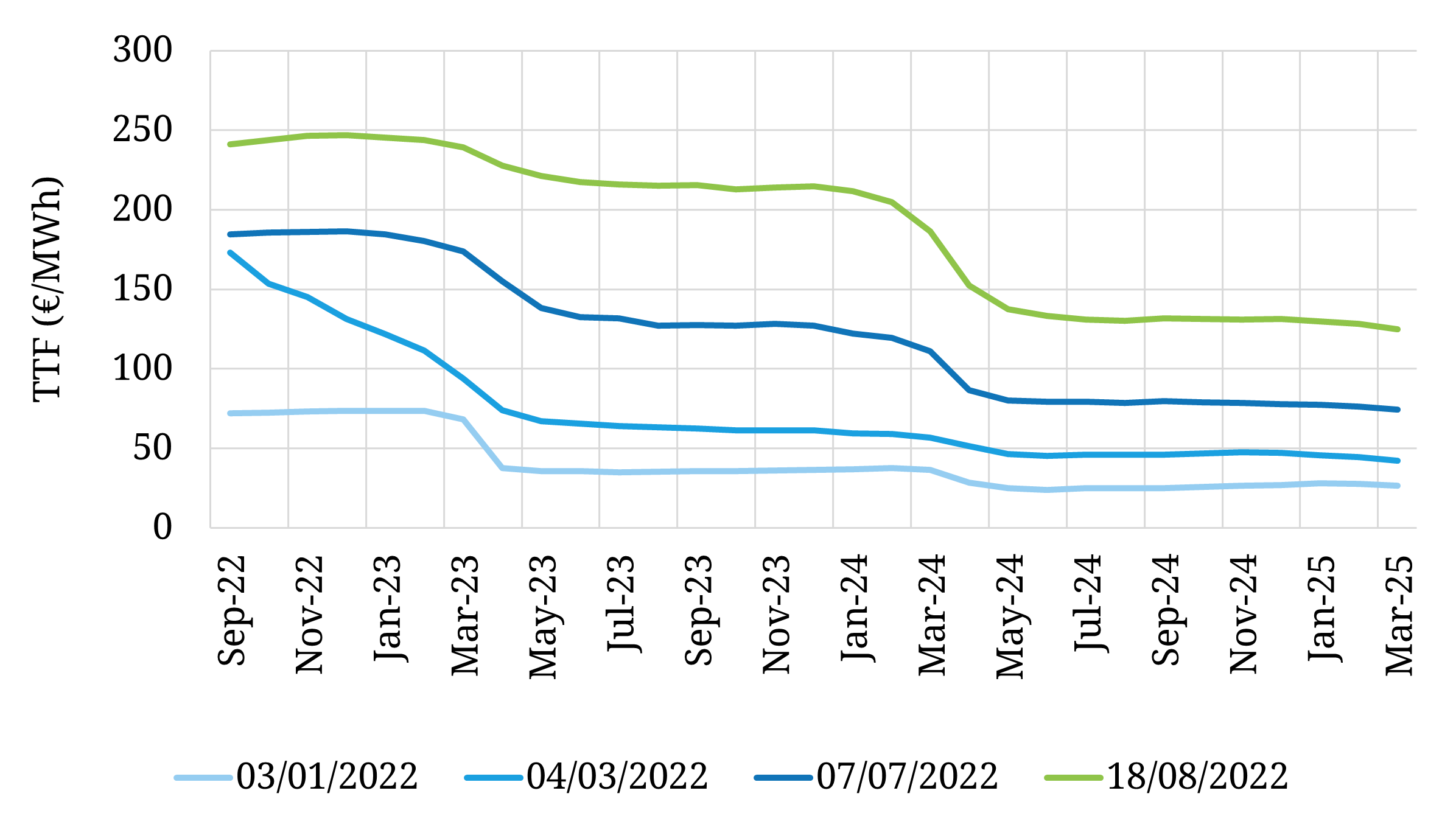

The price of TTF gas for 2023 delivery closed last week above 237 €/MWh (70 $/mmbtu), up 120% since the beginning of July! Power prices rises across the same period were much more aggressive. We’ve run out of adjectives to describe the pace of this price surge.

Acute power market tightness across Europe has been a key factor dragging up forward gas prices across the last 6 weeks. Europe needs more generation output to keep the lights on and the only remaining option is gas.

In today’s article we look at the circular pricing dynamics that are driving an upwards spiral of demand destruction in European gas & power prices.

Forward gas curve surge

We rarely publish the same chart in consecutive feature articles. However to emphasise the scale of the move up in gas prices across the summer, Chart 1 is an update of the chart we showed in July.

Chart 1: The surge in TTF forward prices since early July