Author: Maja Turković, expert in sustainable energy & renewables and country partner on WeBET project

The Western Balkans Energy Transition Dialogue (WeBET) project, together with the NewClimate Institute, has carried out research on the capital cost challenge for renewables in Serbia. Maja Turković, an expert in sustainable energy & renewables and country partner on the WeBET project, reports on findings in an op-ed for Balkan Green Energy News.

Agora Energiewende and think-tank partners from SEE are working together on the project “Western Balkans Energy Transition Dialogue” (WeBET), which aims to assist the countries in the region with renewables policy planning, particularly by addressing current barriers to renewables (RES) deployment, including the high cost of capital for RES financing. One of the activities within the WeBET project was a research project performed with the NewClimate Institute on the capital cost challenge for renewables in Serbia, which was chosen as the Western Balkan case study.

The performed modelling followed the methodology set out in the UNDP Derisking Renewable Energy Investment Report, which was tailored to the specific country context and objectives of the analysis. The quantification of the effectiveness of derisking measures relies on data from structured interviews with private sector investors, project developers and lenders.

RES technologies often face high upfront costs, which make financing conditions highly relevant. The project assessed the impact of financing costs on investment risks in onshore wind projects in Serbia and showed how much financing costs investors and countries could save when advancing national RES deployment with the new de-risking option in the new EU budget framework, accompanied by the implementation of the new RES Directive. Furthermore, it illustrates the potential impact and benefits from a range of policy and financial derisking instruments on the financing costs and consequently the LCOE of wind investments in Serbia.

Barriers to scaling up RES

Renewables are still perceived by financial institutions as riskier and hence they face higher financing and capital costs. Also, higher up-front capital intensity means higher sensitivity to political, regulatory and administrative conditions in the country. The uncertainty regarding future support for renewables contributes to a higher risk perception and may hinder a rapid uptake of renewables in the country. Serbia’s RES support regime is currently undergoing reform, including a revision of incentives and (gradually) moving towards RES support awarded through competitive procurement – auctions.

At the same time, Serbia faces a range of barriers for onshore wind investments, and high costs associated with wind projects’ development – both investment costs with CAPEX reaching 1.5 to 1.6 million EUR/MW, and O&M costs close to 35,000 EUR/MW. While new advancements in the wind turbine technology are expected to drive down CAPEX, the range of barriers are still there which impose risks to investors and hamper RES deployment.

Study results: The cost reduction potential of RES derisking policies in Serbia

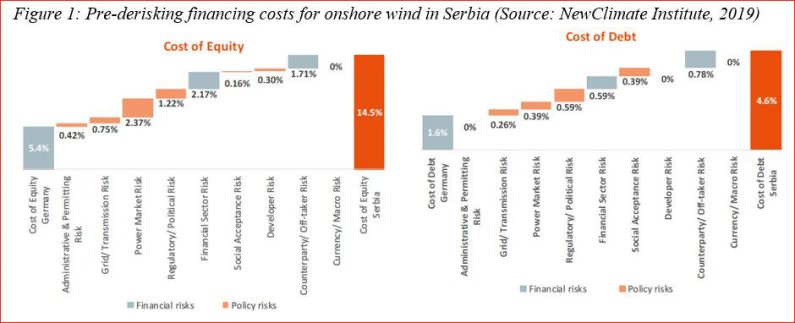

Financing costs for onshore wind in Serbia are high, with a cost of equity (CoE) of 14.5 percent and a cost of debt (CoD) of 4.6 percent, compared to Germany, for example, where financing costs stand at around 5.4 percent and 1.6 percent respectively (Ecofys and eclareon, 2018).

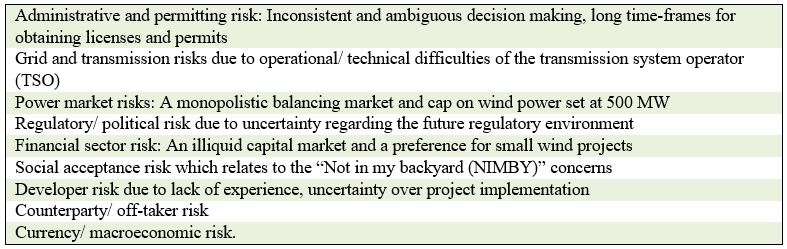

The individual contribution of different risk categories to the increased cost of capital in Serbia were quantified in the model, as shown in Figure 1. In particular, three risk categories are found to significantly contribute to higher financing costs: power market risk, i.e. risks related to the power market regulation, political risk, and counterparty risk – i.e. risk related to the reliability and credibility of the electricity buyer or off-taker. The uncertainty about the future “post-FiT” regulatory framework, restrictions on market development due to a cap on wind power, a monopolistic balancing market, restrictions on off-taker arrangements as well as mixed policy signals on RES developments are the prime drivers behind high risk perceptions and, consequently, high financing costs. Together, the financial risks make up around 3.8 percent points of higher equity financing costs, while policy risks make up 5.3 percent points of higher equity financing costs.

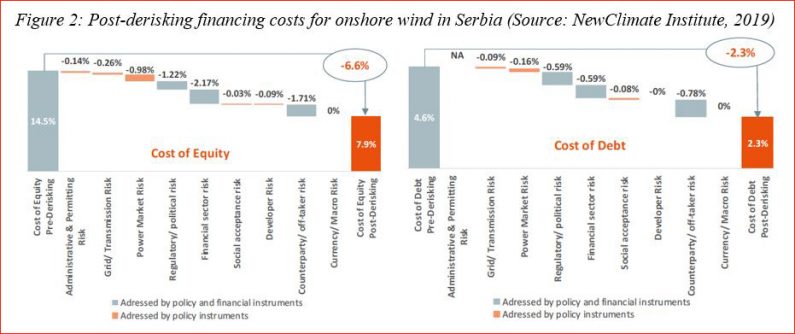

By introduction of a tailored set of public derisking measures, a mixture of policy and financial instruments, financing costs can we lowered. The results show that the financing costs for onshore wind investments could be lowered by 6.6 percent points (CoE) and 2.3 percent points (CoD), as shown in Figure 2.

A RES Cost Reduction Facility, that tackles financial risks, is estimated to be able to reduce the CoE by 3 and CoD by 1.1 percent points. A RES CRF would thus eliminate around 40 percent of the higher cost of capital in the case studied here. Other derisking instruments that could considerably decrease financing costs are a stable and certain RES remuneration scheme and long-term RES targets as well as open and functioning balancing and intraday markets.

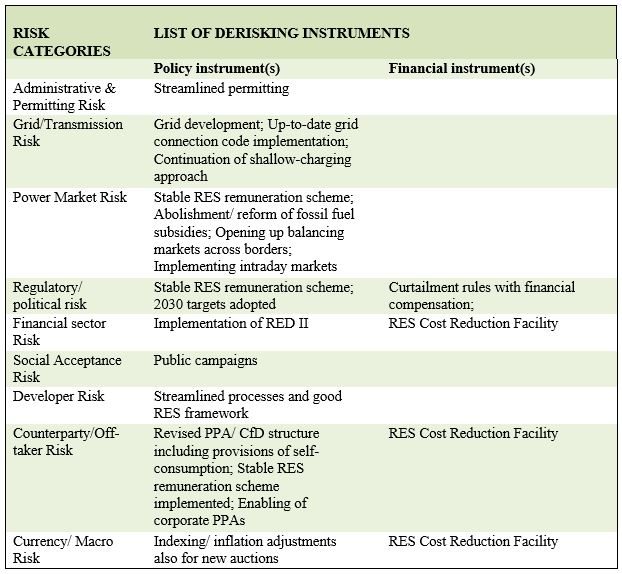

Table 2: Overview RES investment risks and derisking instruments (Source: New Climate Institute, 2019)

The derisking measures also contribute significantly to lower LCOEs for onshore wind (post-derisking). Additional analysis shows that while in a pre-derisking environment, LCOEs for onshore wind are around those for lignite (the technology predominantly discussed in the energy policy context of the country), in a post- derisking environment wind energy generation costs fall well under those for lignite (from 6.7 EUR cents/kWh to 5.5 EUR cents/kWh), a reduction of almost 20 percent compared to 7.3 EUR cents/kWh for new lignite power plant.

This further shifts the attractiveness for a replacement of aging fossil fuel plants to onshore wind parks, provided that the relevant derisking measures are put in place. Furthermore, system efficiencies of below 40 percent and high O&M costs for new lignite power plants increase the risk of the economic viability of those projects. For old power plants O&M costs, along with capital and depreciation costs, will increase over time in correlation with higher investments needed to meet environmental standards. At the same time, risks related to the production of electricity from conventional power sources, such as an increasing CO2 price on fossil fuels which other EU members are already subject to, could also be minimized (Figure 3).

Derisking measures can be an effective tool for policymakers aiming to expand renewable energy capacity in the country. They can have a considerable influence on financing costs for renewables and lowering LCOEs of onshore wind energy by around 20 percent. This offers an additional opportunity for significant cost reductions, going beyond the recent technology cost reductions of renewables with potentially high benefits for taxpayers and consumers.