Foto: iStock

The European Commission has proposed four carbon pricing design options to the contracting parties of the Energy Community – regional market under an emissions trading system (ETS), fixed price ETS, carbon tax and integration into the European Union’s ETS, according to the Impact Assessment for the Establishment of a Regional Emission Trading System in the Contracting Parties of the Energy Community Treaty.

The impact assessment for carbon pricing was presented at a meeting of the Energy Community Ministerial Council in Vienna on December 12.

Ministers representing the contracting parties agreed to analyze the report and communicate the preferred carbon pricing policy scenarios to the European Commission and the Energy Community Secretariat before the next, informal meeting of the Ministerial Council, scheduled for mid-2025.

The Energy Community Secretariat expects the scheme adopted by the end of 2025 in the form of an update to the Energy Community Decarbonisation Roadmap.

Cwetsch: We now enter into the political process

Adam Cwetsch, Head of the Green Deal Unit at the secretariat, said the European Commission presented a list of different options to the contracting parties and that it stressed it isn’t imposing any concrete policy model. The contracting parties have demanded for the report not to focus only on a regional ETS but to go broadly to show the pros and cons of each policy model, he said and added that carbon pricing designs could be mixed in different scenarios.

All the scenarios, in his words, have different potential scopes of carbon pricing. “The analytical process as such has been finalized and now we enter into the political process,” Cwetsch told Balkan Green Energy News.

Some countries have declared their positions. For example, Serbia intends to introduce a carbon tax.

“The contracting parties need to take into consideration the future aspect of joining the EU ETS. It means that what they decide here has to bring them to the trajectory to join EU ETS,” Cwetsch stressed.

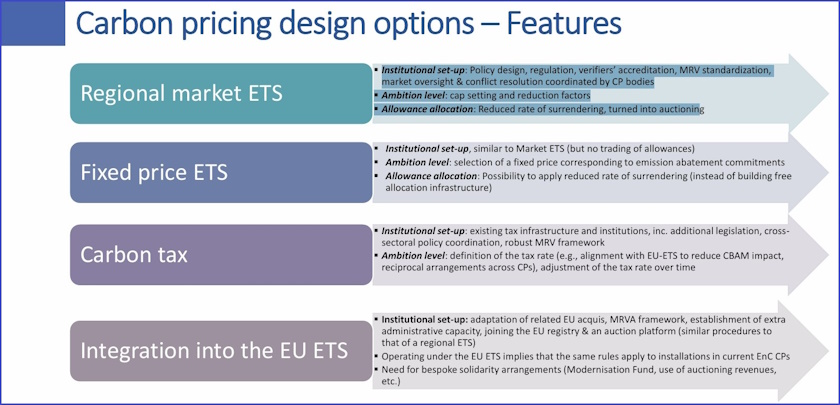

Four design options and three scenarios

The impact assessment has analyzed four carbon pricing design options: regional market ETS, fixed price ETS, carbon tax and integration into the EU ETS. For example, every option has a different institutional set-up, ambition level and allowance allocation.

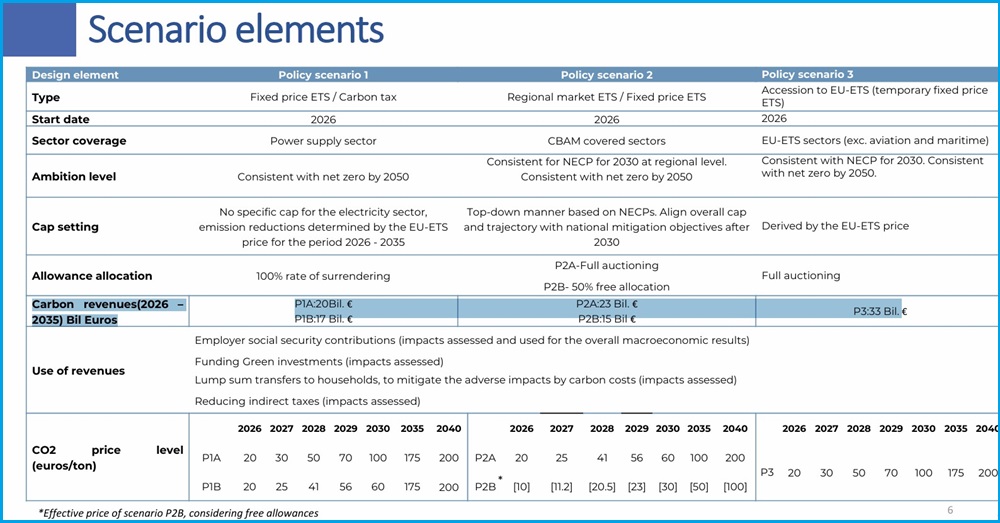

The carbon pricing scheme is modeled in three scenarios, differing in sectoral coverage. The study has designed three main policy scenarios that represent alternative options for carbon pricing, according to the executive summary of the Impact Assessment. Policy scenarios introduce alternative options for carbon pricing starting from 2026. All imply a commitment to drive net greenhouse gas emissions to zero by 2050, according to the presentation.

All three scenarios are compared against a baseline case – status quo

All scenarios are compared against a baseline case, the status quo. It doesn’t include additional carbon pricing policies apart from the ones already enforced by July 2024. The baseline comprises existing policy measures, already in action or announced at the individual level in draft national energy and climate plans (NECPs).

The electricity-only scenario (P1) assumes a single CO2 price for the power sector. It has two pathways: reaching price equivalence with EU ETS by January 1, 2030 (P1A) and a more gradual CO2 price trajectory toward an alignment with EU ETS by 2035 (P1B). The former implies that the electricity sector is exempted from the Carbon Border Adjustment Mechanism (CBAM) for electricity exports. The P1B scenario entails CBAM costs before 2035, as the CO2 price would be lower than in EU ETS.

Under the CBAM sectors scenario, CO2 pricing would be applied to all sectors

Industrial sectors are not subject to any form of carbon pricing at least until 2030 and therefore bear the full cost of CBAM, similarly to the baseline scenario.

Under the CBAM sectors scenario (P2), CO2 pricing will be applied to all sectors, starting in 2026. It also has two versions: a unified CO2 price for all contracting parties required to reach national climate objectives (P2A) and allocating 50% of the allowances free of charge (P2B) for the transitional period until 2035.

The P2A scenario models a unified CO2 price for all contracting parties with the aim of reaching national climate objectives. The price would be at only 60% of the EU ETS in 2030, inconsistent with the CBAM regulation. The carbon price effectively paid would be deducted from CBAM obligations.

The EU ETS scenario (P3) envisages the integration of contracting parties into the EU ETS by 2030 as part of the broader EU accession process. All contracting parties commit to 2030 climate targets, representing a timely pathway to decarbonization.

Carbon revenues in the period 2026-2035 are estimated at EUR 17 billion to EUR 20 billion in the first scenario, EUR 15 billion to EUR 23 billion in the second one, and EUR 33 billion in P3.

A shift from energy-intensive activities to the production of clean energy fuels and other segments

The report’s authors assessed the impact of the scenarios on CO2 emissions, the power sector, the industrial sector, the cost of power generation, climate targets, gross domestic product, and employment.

Under the baseline scenario, the operation of coal- and lignite-fired plants is extended. The gradual increase in carbon pricing in scenario P2 questions the extension of the operational life of coal power plants and halves their generation by 2030.

EU ETS prices in scenarios P1A and P3 lead to an almost complete replacement of coal by 2035. The results in variant P1B are similar to P2 in 2030, but converge to the results of P1A by 2035.

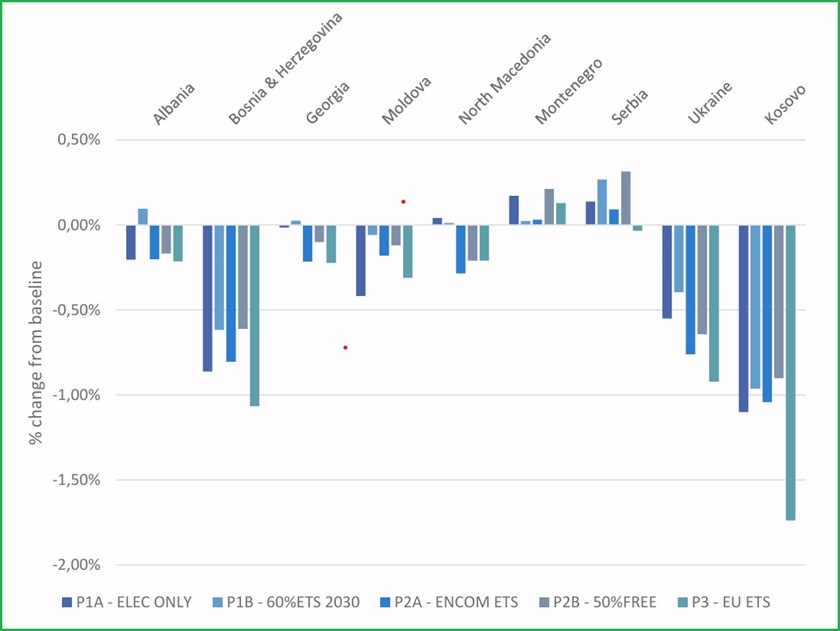

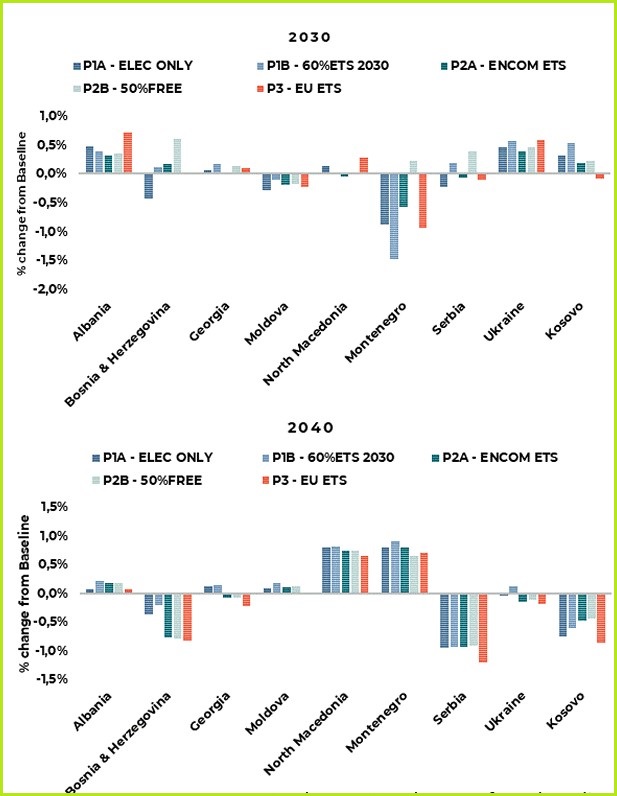

The impact of carbon pricing on GDP is limited

On average, 2030 electricity generation costs are projected at 13% to 29% above the baseline. They are the highest in scenarios P1A and P3 (29%). P1B and P2A show a mildly lower increase (21%) and variant P2B envisages a rise of 13%, according to the study.

Results at the country level reveal a limited impact of carbon pricing on gross domestic product. It is higher in Kosovo*, Bosnia and Herzegovina (due to higher electricity costs), and Ukraine, with cumulative losses for the period 2025-2040 ranging between 0.4% and 1.7% for the three contracting parties.

Smaller impacts are projected for Albania, Georgia, Moldova, North Macedonia, Montenegro, and Serbia. For example, Serbia gets significant gains from higher investments and from recycling carbon revenues.

The most negatively affected activities are associated with power generation from coal

In most of the countries there is a shift from energy-intensive activities to the production of clean energy fuels and other segments, such as the production of consumer goods, the report reads.

All scenarios see employment gains throughout the projection period for most contracting parties. P1B and P2B score best per contracting party and as a whole. The most negatively affected activities are associated with power generation from coal, notably coal mining.

Overall employment losses from 2030 to 2040 are minimal compared to the baseline, fluctuating between 0.5% and 1.5% across scenarios, according to the report.

Be the first one to comment on this article.