By Qendresa Rugova, Burg Capital GmBH, Vienna

esa.rugova@burgcapital.com

This article is part of a series of two articles on energy efficiency investments. The first article covers investment characteristics from a global perspective while the second part focuses on the traditional and emerging financing models for energy efficiency investments.

Global investments in energy efficiency over the past two decades have demonstrated a significant savings potential in energy consumption thereby making a strong environmental and commercial case for efficiency measures. Over the same period there has been an evolution in terms of technological improvements for increased energy savings as well as in the financing mechanisms utilized for energy efficiency investments. This article explores financing models available in developed markets for such investments as well as their applicability in the West Balkan region.

Financing instruments for energy efficiency can be generally grouped into two main categories: A)Traditional financing structures and B)Emerging financing structures (see Figure 1). Driven and championed by policy makers and development banks, traditional financing structures have been instrumental in demonstrating the benefits of energy efficiency measures from both policy-making and commercial perspectives. Such financing models are rather straightforward and have a longer track record.

However, despite the demonstrated benefits, traditional financing instruments are not always successful in creating the necessary demand to deploy investments at the required scale. To address such aspects, further innovative structures have emerged in developed countries aiming at addressing some of the investment hurdles summarized in Part 1. Examples of structures from each category are indicated in Figure 1 while each structure is briefly explained below.

Figure 1: Traditional and emerging financing structures for energy efficiency investments (Source: Burg Capital)

Traditional financing models

Dedicated credit lines (soft loans) – credit lines for energy efficiency measures extended to end users at preferential terms in terms of maturity and/or interest rates. Such credit lines are often provided by national or international development banks (such as European Investment Bank (EIB) and European Bank for Reconstruction and Development (EBRD) and are further distributed to designated markets through regional partner retail banks.

Risk-sharing facilities – mechanisms used to enhance the credit aspect of a certain instrument for example through guarantee funds or first-loss facilities. Such enhancements typically reduce the level of risk for financiers of equity investors by covering a specific part of the risk (e.g. a specified rate of default rate).

Leasing –similar to other lease-financing structures for products such as cars, leasing may be used for energy efficiency. Financing is provided for specific equipment whereby the end user rents (leases) that particular equipment from the lessor.

Covered bonds – highly regulated class of bonds that enjoys superior credit ratings due to a dual recourse structure as compared to other unsecured issued debt. Such bonds are backed by actual assets (cover pool), for example in the case of mortgage lending, as well as the general backing of the issuing entity. In the case of energy efficiency, the “cover pool” is comprised of a portfolio of energy efficiency loans which are used as collateral for the bond.

Real estate and infrastructure funds are well established structures for investing in real estate and infrastructure projects through funds which are set up for the sole purpose of finding suitable projects that are aligned with the fund’s strategy. In terms of energy efficiency, such funds provide for a great vehicle to invest in efficient real estate projects, though the energy efficiency component is not specifically defined and reported and, as such, it is often “hidden” in the investment.

Energy Performance Contracting (EPC) – allows Energy Saving Companies (ESCOs) to undertake the implementation of energy efficiency measures on behalf of the end user through an Energy Performance Contract (EPC), which often provides a guaranteed level of energy savings to the beneficiary and furthermore allows for a sharing of future energy savings between both parties.

There are two distinct types of EPC contracts, the “financing Energy Performance Contracts” and “operational Energy Performance Contracts”. The key difference lies in the arrangement of financing. In operational EPCs the user is the borrower and the financing agreement is entered between the user and the lending institution on the basis of the EPC. In this case, ESCO’s role is more operational, which mitigates technical-related risks and by acting as savings guarantor.

In financing EPCs ESCOs originate the project, arrange third party financing, implement the efficiency measures and monitor the project. For large projects, such a centralized role is extremely beneficial as the ESCO serves as the main counterparty role for the financiers as well as the beneficiaries.

Emerging financing models

On-bill repayment – mechanism that allows end user to benefit from energy efficiency investments without having to incur up-front costs. Investments are made typically by the utility company or a third party financier, while the repayment is done by charging a repayment fee on the monthly utility bills. This structure leverages the existing relationship between the utility company and the customer and the default rates are usually very low.

On-tax finance – structure introduced in the U.S also known as the Property Assessed Clean Energy (PACE) which allows municipal authorities or private financiers to extend loans to property owners for energy efficiency investments. Loans are attached to the property which is being financed and the loan is repaid via local taxes. Similar to the on-bill financing, this structure results in a very low default level as the repayment is linked to taxes.

Energy efficiency funds – designated vehicles for energy efficiency investments typically set up with private or public funding or a combination thereof. Investment principles are set by the fund and projects are targeted based on a set return. In essence, the fund functions much like any other infrastructure fund whereby there is a fund manager as well as other investment advisors appointed to assess investment opportunities. Such funds may place investment in various energy efficiency projects that may use energy performance contracting or any other suitable mechanism. At the European level, there are many examples of such funds, such as the European Energy Efficiency Fund (EEEF), aiming to help EU member countries achieve the 20% target. Investments may be placed directly to a project or channeled through intermediary banks.

Revolving funds (internal) –are mechanism used by organizations (companies, NGOs, municipalities, universities) to fund ongoing measures in energy efficiency. In such structures a certain amount of capital is set aside to fund internal efficiency projects and the fund is constantly replenished by the savings generated from the projects already invested.

Green bonds – emerging instrument with proceeds which are designed to be used to fund climate investments i.e. projects that aim to reduce greenhouse gas emissions or are geared for other sustainability related purpose. In essence, green bonds are similar to normal corporate bonds but carry a green element, which makes them distinct in how proceeds are used.

While the asset class is increasingly becoming more attractive and utilized globally (USD 50 billion green bonds issued in 2015), there are still many issues that need to be addressed, such as setting up the principles and standards across various industry segments including energy efficiency to allow for such instruments to go mainstream. The Climate Bond Initiative is a non-profit organization that is championing the use of such instruments to mobilize bond financing for climate-related projects.

ESA financing model –emerging structure based on the traditional project finance model for energy projects. A project developer (Sponsor) establishes a Special Purpose Vehicle (SPV) for the purpose of arranging, owning, operating and financing the energy project, in this case energy efficiency projects. ESA is an evolution of EPC seen in ESCO structures, but the revenue aspect mimics the Power Purchasing Agreements (PPA), seen in energy generation projects. In the case of energy efficiency, SPV and the end user enter into an ESA based on which the end user pays the SPV for the actual energy saved, either as a fixed dollar amount per kWh saved or a floating amount based on a percentage of the utility bill.

Public ESCOs for deep renovation – financing structure that combines the EPC concept with a publicly owned SPV set up with the purpose of funding and owning energy efficiency projects implemented in public buildings. Such a structure is typically set up with public funds and targets projects with deep refurbishment ambitions. Such setups are also designed with public procurement rules in mind.

Community funding – bottom-up approach of instrument that sources funding for renewable or energy efficiency investments from local communities where such investments would take place. These structures allow communities to partake in local projects through which they receive the given financial returns as well as the environmental and economic benefits of achieved energy savings.

Secondary markets – one of the means of providing capital liquidity for ESCOs or other holders of energy efficiency debt is the creation of a secondary market for energy efficiency investments, whereby portfolios of loans or initially issued in a primary market are able to be packaged into a loan portfolio or tradable securities such as bonds or asset-backed securities that are in turn sold in secondary markets. Secondary markets, lower overall transaction costs, promote liquidity by providing financiers an exit strategy and a transparent and reliable market price, thus increasing the number of lenders willing to participate in this market. Such investors may include private capital sources of pension funds, insurance companies, private equity and so forth. To date, two transaction structures have been observed: loan portfolio sales and bond sales, which are further categorized as revenue bonds or asset-backed securitizations. One example of a successful use of secondary transaction model is observed in Bulgaria whereby the Bulgarian Energetics and Energy Savings Fund (EESF) acts as a secondary buyer of future receivables from EPCs from ESCOs. This financing method enables ESCOs to free up their balance sheet to be able to develop and fund a new source of projects.

The secondary market for energy efficiency loans is at the very early stage of development. Market uptake for energy efficiency projects is constrained by low demand for energy efficiency project pipeline, on one hand, and consequently limited appetite to finance such projects. However, in order to reach the necessary scale and meet the policy targets, development of secondary markets is imminent to finance energy efficiency at scale.

Energy efficiency in the West Balkan region – potential and financing

A report recently published by the Energy Community on the potential of energy efficiency in the Energy Community Contracting Parties looks at the potential for energy efficiency in the Western Balkans as well as the available funding options for such investments.

The study presents an important finding regarding the region’s high energy intensity as compared to the EU. Energy intensity indicates the amount of energy a particular country or region uses to produce one unit of gross domestic product (expressed in tonnes of oil equivalent per million dollars). The West Balkan region is 2.5 times more energy intensive than the EU mainly as a result of obsolete state of the energy infrastructure, high distribution losses as well as low energy efficiency in the end user sector, particularly in industry and buildings. Such high energy intensity signifies an immense potential for energy savings through various technological improvements. The study points out a significant potential for increasing energy efficiency particularly in the buildings sector which represents 50% of total energy consumption with an estimated potential for energy savings between 20% and 40%, yielding up to EUR 805 million by 2020.

Energy potential in sectoral terms for the region is as follows:

- Transport: 10%

- Household sector: 10-35%

- Public: 35-40%

- Service sector: 10-30%

- Industrial and commercial: 5-25%

Financing of energy efficiency investment in the Balkans is at the very early stage of development and, as such, it is still going through the preliminary phases of increasing awareness about the benefits of energy efficiency, regulatory reforms, as well as showcasing successful examples of energy efficiency projects. Such projects have been predominantly financed through dedicated credit lines and, in some cases, also through regional energy efficiency funds that have been established by various multilateral institutions. Some of examples of such funds are the Green for Growth Fund (GGF), specialized for investing in energy efficiency and renewable energy projects in Southeast Europe including Turkey, and the Regional Energy Efficiency Programme (REEP) for the Western Balkans, initiated by the European Commission with MFIs as partners (CEB, EBRD, EIB) for the purpose financing energy efficiency projects helping countries to reach their sustainable energy objectives. Both funds offer technical assistance grants for establishment of the regulatory framework as well as removing policy barriers.

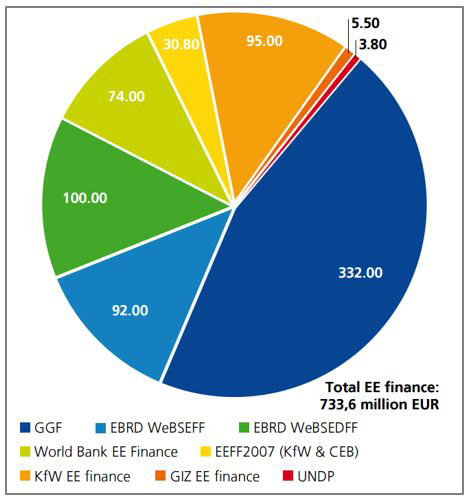

A study initiated in 2015 by the IFI Coordination Office has identified eight regional programmes offering financial and/or technical assistance to improve energy efficiency in the Western Balkans. The total amount of funding from all available sources comes to over EUR 733.6 million. A breakdown of funding by institution is presented in the figure below.

Figure 2: Energy efficiency facilities in the Western Balkans in the first quarter of 2015 (in millions of euros), Source: Energy Community

In general, availability of funding is not considered to be the biggest impediment to increasing energy investments in the region. The biggest barriers continue to be those pertaining to the regulatory uncertainty as well as the lack of required capacity to build a strong project pipeline.

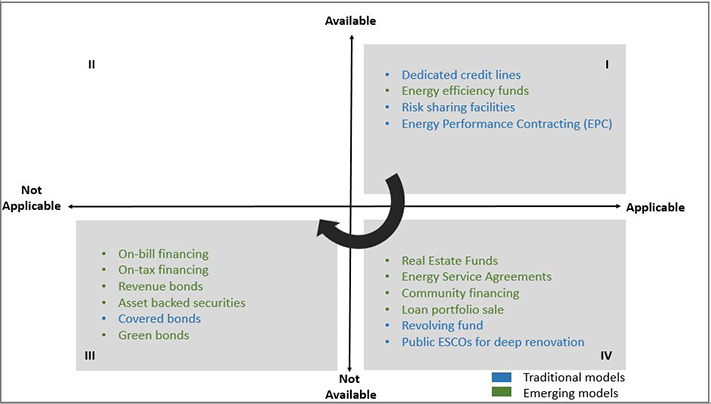

Having looked at the traditional and emerging financing options in developed markets and the available funding in the West Balkan region, it is worthwhile to look into how such available structure could be adopted and utilized in the future. Firstly, it is fair to say that the energy efficiency market will continue to be predominantly funded through the existing models of credit lines and direct investments into projects. However, as the region reaches the necessary regulatory milestones in terms of harmonizing the relevant legislation with the EU directives, it is important that alternative scenarios are also explored in order to understand options and stay up to date with the lessons learned from other developed markets.

The figure below outlines the possible financing structures in terms of availability and applicability in the Balkan region. The most obvious development path is to further strengthen the deployment of funding through available structures. Though placed in the first quadrant, the EPC structure is currently at the very early stage of adoption via the establishment of ESCOs. It is of outmost importance that this structure is properly utilized and creditworthy and that competent ESCOs are established in the region. This would allow for transfer of skills in terms of the technical know-how for the necessary Measurement, Verification and Reporting processes.

As necessary skills are established, other options (Quadrant IV) could be considered such as the establishment of revolving funds in particular organizations, or possible sale of loan portfolios (like in the Bulgarian example) to a secondary buyer to allow for future investments to take place. Public ESCOs, which are being implemented in France, are also a good option for tackling publicly owned buildings. Available grants should be also sought to be coupled with such structures to lever private funding.

Quadrant III contains the options that are least likely to be applied due to the fact that they are relatively novel in developed markets and that in principle they require properly developed capital markets and significantly large projects. On-bill financing could be used, however local utilities’ ability to secure the necessary capital to undertake such projects on behalf of users is uncertain.

Figure 3: Possible development roadmap for funding of energy efficiency in the West Balkans (Source: Burg Capital)

The need for investment in energy efficiency and economic upside from doing so is most pertinent in West Balkans due to very high energy consumption intensity. While availability of funding could be considered a challenge, the biggest impediments to further improving energy efficiency in the region are regulatory uncertainty and the lack of required capacity to build a pipeline of projects.

The region could draw on the experience of Western Europe in adopting already existing and prove traditional models of energy efficiency financing. With the gradual establishment of the necessary skills on the local level, combined with the further advancement of energy efficiency financing mechanisms on a global level, the West Balkan region could transition to adopting the emerging models outlined in this article.

Qendresa Rugova is a Senior Consultant at Burg Capital – a corporate and project finance advisory firm. She specializes in renewable energy, emerging trends in clean technologies and financing models.

References

- Bloomberg, Hirtenstein Anna, ‘Bond Market Asking: What is Green – Curbs Climate Friendly Debt’ March 2016

- Bullier Adrien, Milin, Christophe, Alternative financing schemes for energy efficiency in buildings, 2013

- Energy Efficiency Financial Institutions Group (EEFIG), Driving New Finance for Energy Efficiency Investments Summary for Institutional Investors of the work of the Energy Efficiency Financial Institutions Group (EEFIG), May 2015

- European Commission, Joint Research Centre, Institute for Energy and Transport, ‘Energy Performance Contracting’, 2015

- Energy Community Secretariat, ‘Energy Community – Tapping on its Potential Energy Efficiency Potential’, June 2015

- Hull, Jeanine, Strategic Energy Advisors, ‘The Role of State, Local, Territorial and Tribal Governments in Energy Efficiency Loan Markets’, January 2010

- Kats Greg, ‘Energy Efficiency Financing – Models and Strategies’, October 2011

- State and Local Energy Efficiency Action Network, Accessing Secondary Markets as a Capital Source for Energy Efficiency Finance Programs: Program Design Considerations for Policymakers and Administrators, Financing Solutions Working Group, February 2015

- Wilson Sonsini Goodrich & Rosati, Innovations and Opportunities in Energy Efficiency Finance, May 2012

- Zimmerman, Greg, Facilitiesnet, ‘Financing Tools Include Energy Performance Contract, Energy Service Agreement’, March 2015