Authors: Danko Kalkan, Manager of ESG team, and Katarina Kulić, Senior in ESG team, EY Serbia

The sustainable development phenomenon goes the way from that it is good for the reputation to bringing materially significant risk to that it is a more and more complex legal obligation.

What is making ESG, as a sustainable development framework, one of the main factors in decision making in companies? What do the new European directives entail? What implications can it have on our region and how to prepare?

Increasing significance of ESG in decision making

Cimate-related, environmental and increasing social challenges are putting pressure on decision makers from different spheres and on different levels to provide comprehensive systemic solutions. Environmental protection measures and socially responsible business operations aren’t strictly linked to reputation building anymore as the aforementioned challenges become materially significant risks for companies.

Therefore it is no surprise that environmental, social and governance (ESG) factors are becoming dominant in decision making in the corporate world. ESG factors are a set of criteria that businesses and investors use to assess the level of sustainability and ethics in their operations, activities and investments. ESG can be seen as a comprehensive framework that unites the most important issues in the process of sustainable development implementation.

Effect of global megatrends

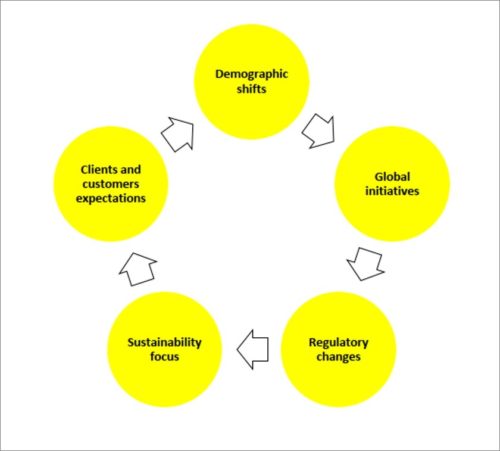

There are five main reasons that ESG factors are being included more and more in the decision making processes. First, there are global demographic changes as the baby boomer generation is retiring and passing its wealth on younger generations which, being aware of the inherited environmental and climate-related challenges and the need for efficient solutions in a limited timeframe, have a completely new angle on sustainable development.

Second, we are witnessing an increasing number and volume of global initiatives, deriving directly or indirectly from the Paris Climate Accords, United Nations Sustainable Development Goals and other similar endeavors. The said initiatives have an effect on the national and corporate levels, and the level of tracking the success of implementation is getting more intensive. With regard to that, all market participants are being urged to include the consideration of ESG factors into their governance processes, so the rising trend of defining new sustainable development regulations, led by the European Union, isn’t surprising.

In that sense, for instance, there are notable requests to make nonfinancial reporting (reporting that doesn’t necessarily include financial indicators, but it gives stakeholders information on the value of the company outside of the financial reporting frame) an integral part of annual reports.

Further on, sustainable long-term investments are becoming the main focus point for capital holders and private markets. It is the main reason that the capital allocated for ESG strategies is increasing. Also, the biodiversity preservation issue is becoming more and more important while socio-economic factors are becoming part of the risk management process. Finally, the expectations of the consumers and users of services have changed. We see rising skepticism and the need for increased transparency regarding the impact of companies and their products on the world around us.

EU’s sustainable development action plan and taxonomy

Back in 2018, the European Commission defined its Action Plan on Financing Sustainable Growth and determined its three main objectives:

- Reorienting capital flows toward a more sustainable economy,

- Mainstreaming sustainability into risk management,

- Fostering transparency and longtermism

One of concrete steps in the implementation of the plan is defining the European taxonomy. The classification system is envisaged to establish a common language and nomenclature for economic activities and their contribution to environmental goals. The taxonomy’s main purpose is indeed to meet the first goal of the Action Plan on Financing Sustainable Growth. Also, the regulatory set’s important objectives are also to avoid greenwashing, enable easier decision manking and set the foundations for other directives concerning sustainable development.

The EU taxonomy’s criteria were published for the first two climate-related goals (mitigation and adaptation) while they are expected to be published during this year for the remaining four goals.

Companies from the nonfinancial sector are obligated to report on the compliance with the taxonomy’s criteria from January 1, 2023. In the meantime, only the qualified activities are reported.

The obligation to report on the compliance with regard to all six goals for the financial sector comes into force on January 1, 2024. In the meantime, reporting is required only on the key sectors covered by the EU taxonomy. By then, the new nonfinancial reporting directive is expected to be long established, together with the first European reporting standard, and they will stipulate the obligations in detail.

Proposal for new nonfinancial reporting directive

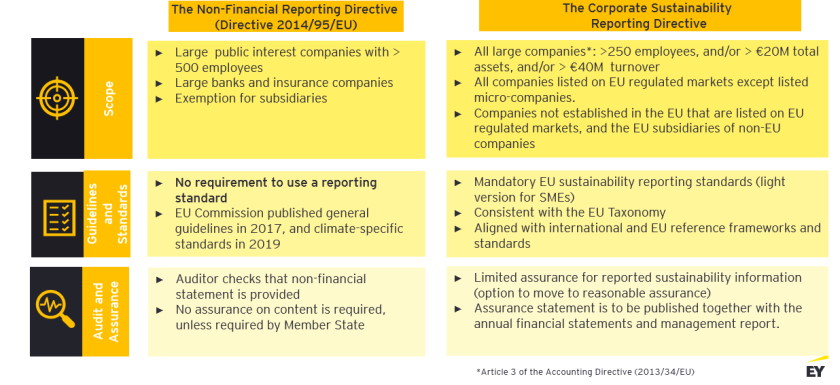

As for the third goal of the said action plan, concerning increased transparency, the European Commission published in April of last year the proposal for the new nonfinancial reporting directive – Corporate Sustainability Reporting Directive – CSRD, which should replace the existing Non-financial Reporting Directive – NFRD.

The purpose of the change in the regulations is to harmonize sustainability reporting with financial reporting and cover many more companies than with the existing NFRD. It is estimated that CSRD would impose the obligation on 49,000 companies to publish data and information about their effect on sustainable development, a considerable change and increase from the current 11,600 entities covered by NFRD.

The second objective of the new regulations is to establish consistency in nonfinancial reporting that should enable investors and the general public to get insight into comparative and reliable information on sustainability, reducing potential greenwashing, which is now present at a very large scale. Finally, the new regulations bring an important change with a requirement for the published information to be verified by independent auditors, which adds weight and importance to the whole process.

According to article 8 of the EU taxonomy, all companies that have obligations under the NFRD (directive 2014/95/EU) must publicly disclose information on the way and how much their activities affect sustainable development. In particular, companies are required to report through three indicators – income, capital investment and operating expenses related to green activities.

As for the financial sector, the aforementioned article 8 didn’t define specific indicator for the entity class. It is why in 2020 the European Commission asked the European Banking Authority to propose a way for banks to report on the share of green assets in their balance sheets. In connection with that, EBA proposed the so-called green asset ratio (GAR) indicator. It is supposed to reveal the share of financial institutions’ assets that is environmentally sustainable and is significantly contributing to climate-related goals (adaptation and mitigation) or enabling the achievement of the goals with other activities.

In addition to particular indicators, all companies covered by the directive will have to describe their business models, strategies and policies as well as their sustainable development goals and the ways to monitor them. Furthermore, it will be required to report on the management of key environmental and climate risks. Finally, companies will have to describe their administrative and governance capacities in the same context.

Main implications of these changes for the business sector

Given everything that has been mentioned so far, the obvious conclusion is that companies will have to disclose more data and information than ever before including the information that was so far considered sensitive (especially with regard to the business model, strategies and supply chains). The information will have to be prepared by using complex processes of measuring and reporting, and all the published information will be verified by third parties.

In order to fulfil all the requirements from the upcoming nonfinancial reporting regulations, companies will have to make more effort to bring significant changes to the way they manage systems and collect information.

However, the changes shouldn’t be seen only as an additional burden for the process. Namely, the said novelties enable companies to consider changing their business models and the way they manage and utilize resources, which is an opportunity to achieve long-term savings and get new business opportunities.

The new directive’s potential implications in the region

The existing European NFRD (directive 2014/95/EU) has been transponed into Serbian and Montenegrin legislation through their laws on accounting. All big legal persons of public interest and those with over 500 employees are obligated, under the two countries’ laws, to publish nonfinancial reports.

However, there are notable challenges within the organizations concerning the production of the said reports. The challenges regarding an adequate distribution of tasks in the collection of adequate information are especially discernible, which points to a lack of a systemic approach to the challenge.

It surely takes certain time for the companies to adapt to legal changes. However, the European Green Deal imposes more and more requirements for the implementation of sustainable development in business activities. Given that, by signing the Sofia Declaration on the Green Agenda for the Western Balkans, the countries of the region have recognized the European Green Deal as the European Union’s new strategy for the continent’s sustainable future, all the changes in EU regulations that were mentioned will unavoidably be applied in the Western Balkan region, too.

How to prepare for changes in time?

In order to prepare for the upcoming changes, companies will have to revise the existing strategies, policies and objectives as soon as possible to define new ESG action plans with measurable short- and long-term goals and success indicators. The step can include revising and redefining the companies’ basic values and, possibly, changes to their business models.

Then, in order to monitor and, if necessary, adjust the set goals, it is necessary to establish an adequate organizational structure and mobilize the needed human and material resources. Within the structured system, it is also required to define the procedures and processes that will enable sustainable management and monitoring of the processes. A system set up this way enables an efficient and purposeful collection of the ever more demanding data and information on ESG and enables companies to comply more easily with the existing and upcoming legal obligations.

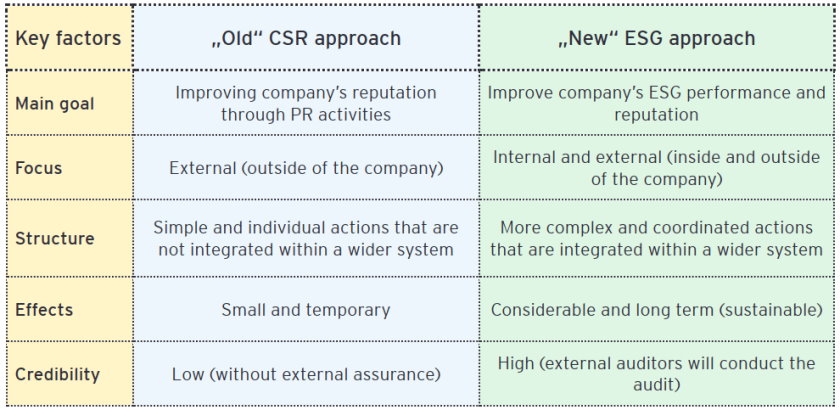

The final product of a systemic approach should be a new ESG approach that differs significantly from the approach used so far, where marketing and PR approach was dominant.